The Complete Financial Planning Blueprint: How to Build Net Worth and Achieve Lasting Wealth

A step-by-step framework used by Certified Financial Planners — adapted for individuals who want to take control of their financial future, starting today.

By EDUNXT TECH LEARNING — a pioneer in EdTech solutions, AI-powered educational services.

Why Financial Planning Is the Foundation of Wealth

Every individual who has ever achieved lasting financial independence started from the same place: a decision. Not a windfall, not a lucky trade, not a single extraordinary year of income — a decision to stop treating money as something that simply happens to them and start treating it as something they actively design. Planning your financial future and growing your net worth requires discipline, commitment, and consistency. It is not an overnight process. It is a compounding one, built quarter after quarter, decision after decision, until the results become undeniable.

At a global fintech and investment level, we see this pattern repeat across every market, every currency, and every income bracket: people who build wealth are not necessarily the people who earn the most. They are the people who plan the most deliberately. This guide exists to give you that plan — a professional, structured, and repeatable system for understanding where you stand financially, where you want to go, and exactly how to get there.

This is not a theoretical presentation. It is designed to function as a standard operating procedure (SOP) — a document you can return to at every stage of your financial life, whether you are opening your first savings account or restructuring a seven-figure portfolio. We will walk through six practical, sequential steps to grow your net worth, then step back and examine the deeper architecture of wealth: the four lifetime pillars, the professional six-step planning process used by Certified Financial Planners (CFPs), the discipline of record-keeping, and the goals that most commonly drive people to seek financial guidance in the first place.

Before we go further, it’s worth being honest about something the finance industry rarely says out loud: most people are not naturally good at this. Most people are, by nature, poor long-term planners and excellent short-term procrastinators. That is not a character flaw — it is a well-documented feature of human psychology. We are wired to prioritize immediate rewards over distant ones, which is precisely why an unstructured approach to money so often fails. The solution isn’t willpower. It’s a system. That is what this guide provides.

1Determine Your Net Worth

The first step in planning your financial future is to determine your net worth. Your net worth is the single most honest number in personal finance — the difference between everything you own and everything you owe. It is calculated with a simple formula:

Net Worth = Total Assets − Total Liabilities

To calculate it accurately, begin by listing every asset you hold. This includes liquid cash in checking and savings accounts, investment holdings such as stocks, bonds, mutual funds, and retirement accounts, real estate you own (including your primary residence), vehicles, and any significant personal property such as jewelry, art, or collectibles that carry resale value.

Next, list every liability. This includes mortgage balances, credit card debt, student loans, auto loans, personal loans, and any other outstanding obligations. Once both lists are complete, subtract total liabilities from total assets. The resulting figure — positive, negative, or near zero — is your true financial starting point.

Why This Number Matters More Than Your Salary

Income is a flow; net worth is a stock. A high salary with high liabilities can produce a lower net worth than a modest salary paired with disciplined saving and low debt. Many professionals who appear financially successful from the outside — driving expensive cars, living in premium neighborhoods — carry a fragile or even negative net worth once liabilities are accounted for. Knowing your net worth strips away appearances and gives you an unambiguous baseline to measure every future financial decision against.

Professional tip: Recalculate your net worth on a fixed schedule — quarterly is ideal, annually at minimum. Trend lines matter more than any single snapshot. A net worth tracker (spreadsheet or app) that shows the trajectory over 12–36 months is one of the most motivating tools in personal finance, because progress that feels invisible day-to-day becomes obvious over a year.

2Set SMART Financial Goals

Once you know where you stand, the next step is deciding where you’re going. Vague ambitions like “I want to be rich” or “I want financial freedom” are not goals — they are wishes. Effective financial goals follow the SMART framework: they are Specific, Measurable, Achievable, Relevant, and Time-bound.

| SMART Element | Weak Goal | Strong Goal |

|---|---|---|

| Specific | “Save more money” | “Save for a home down payment” |

| Measurable | “Pay off debt” | “Pay off $12,000 in credit card debt” |

| Achievable | “Save $50,000 this year on a $40,000 salary” | “Save $6,000 this year (15% of income)” |

| Relevant | A goal unrelated to your actual priorities | A goal tied to retirement, family, or security |

| Time-bound | “Someday” | “Within 24 months” |

Common examples of well-formed financial goals include saving for a down payment on a home, systematically paying off student loan debt, or building a retirement portfolio that replaces a target percentage of current income. Once goals are written down, the next task is prioritization — ranking them by both importance and urgency, since very few people have the resources to pursue every goal simultaneously at full intensity.

Long-Term, Medium-Term, and Short-Term Horizons

Professional financial planners typically organize goals into three time horizons:

- Short-term (1–5 years): Emergency fund completion, a vacation fund, a vehicle purchase, or paying off a specific debt.

- Medium-term (5–10 years): A home down payment, funding a portion of a child’s education, or launching a business.

- Long-term (10+ years): Retirement income, estate planning, and generational wealth transfer.

Writing goals down in each category — with real numbers attached — converts an abstract desire for “wealth” into a concrete, trackable roadmap.

3Build a Working Budget

A budget is the operating system of financial planning — every other step runs on top of it. Creating a budget is crucial to achieving your financial goals because it forces visibility into where money actually goes, rather than where you assume it goes. Begin by listing total monthly income from all sources, then list every category of expense: housing, food, transportation, insurance, debt payments, and discretionary spending such as entertainment and dining.

Once both sides are laid out, compare income to expenses and identify categories where spending can be reduced without materially harming quality of life. Crucially, your financial goals from Step 2 should be built directly into the budget as non-negotiable line items — treated with the same seriousness as rent or a loan payment, not as an afterthought funded by whatever happens to be left over.

A widely used starting framework: the 50/30/20 rule. Allocate roughly 50% of after-tax income to needs (housing, utilities, groceries, minimum debt payments), 30% to wants (dining out, entertainment, subscriptions), and 20% to savings and additional debt repayment. This is a starting point, not a rigid law — adjust the ratios to match your income level, cost of living, and goal timeline.

Pay Yourself First

The single highest-leverage budgeting habit is automating savings the moment income arrives, rather than saving whatever remains at month-end. When savings are automatic — moved to a separate account before the money is ever “seen” in a spendable balance — the discipline required drops dramatically, because there is no daily decision to make.

4Create an Emergency Fund

Unexpected expenses can derail even the most carefully constructed financial plan, which is why an emergency fund is treated as a non-negotiable priority, not an optional extra. The standard professional guidance is to hold three to six months’ worth of essential living expenses in a separate, easily accessible savings account — not invested in the market, not locked in a fixed deposit with early-withdrawal penalties, but liquid and immediately available.

This fund exists for one purpose: to absorb shocks — a medical bill, a job loss, an urgent home or vehicle repair — without forcing you into high-interest credit card debt or derailing progress on your other goals. Individuals with variable income (freelancers, commission-based earners, business owners) should lean toward the higher end of that range, sometimes extending to nine or twelve months, given the greater unpredictability of their cash flow.

Build it in stages: If six months of expenses feels unreachable, start with a “starter fund” of one month, then $1,000, then gradually build toward the full target. An incomplete emergency fund is still dramatically better than none — even partial coverage prevents many financial setbacks from becoming financial crises.

5Eliminate High-Interest Debt

Paying off debt is one of the most direct ways to grow net worth, because eliminating a liability has the same mathematical effect on your balance sheet as growing an asset. Start by making minimum payments on every debt to remain in good standing, then direct all additional available money toward the debt carrying the highest interest rate — commonly known as the debt avalanche method. Once that balance is cleared, redirect the freed-up payment toward the next-highest-rate debt, and continue until all debt is eliminated.

| Strategy | How It Works | Best For |

|---|---|---|

| Debt Avalanche | Pay off highest interest rate first | Minimizing total interest paid |

| Debt Snowball | Pay off smallest balance first | Building psychological momentum |

| Debt Consolidation | Combine multiple debts into one lower-rate loan | Simplifying payments, reducing rate |

The mathematically optimal approach is the avalanche method, since it minimizes total interest paid over time. However, some individuals find the debt snowball method — paying off the smallest balance first regardless of interest rate — more sustainable, because early “wins” build the psychological momentum needed to stay disciplined through a long payoff journey. The best method, ultimately, is the one you will actually stick with.

6Invest for Long-Term Growth

Investing is the engine that transforms disciplined saving into genuine wealth. Saving alone, even done consistently, is generally insufficient to outpace inflation and build meaningful long-term net worth — this is where a structured investment strategy becomes essential. Consider tax-advantaged retirement vehicles such as an Individual Retirement Account (IRA) or an employer-sponsored retirement plan, alongside taxable brokerage accounts for goals outside of retirement.

Diversification Is Non-Negotiable

Make sure to diversify your investments across asset classes, sectors, and geographies to minimize concentration risk. A portfolio overly weighted in a single stock, sector, or asset type is vulnerable to shocks that a diversified portfolio can absorb. The specific mix of equities, bonds, real estate, and alternative assets should reflect your time horizon, risk tolerance, and financial goals — a 30-year-old investing for retirement can typically absorb more volatility than someone five years from retiring.

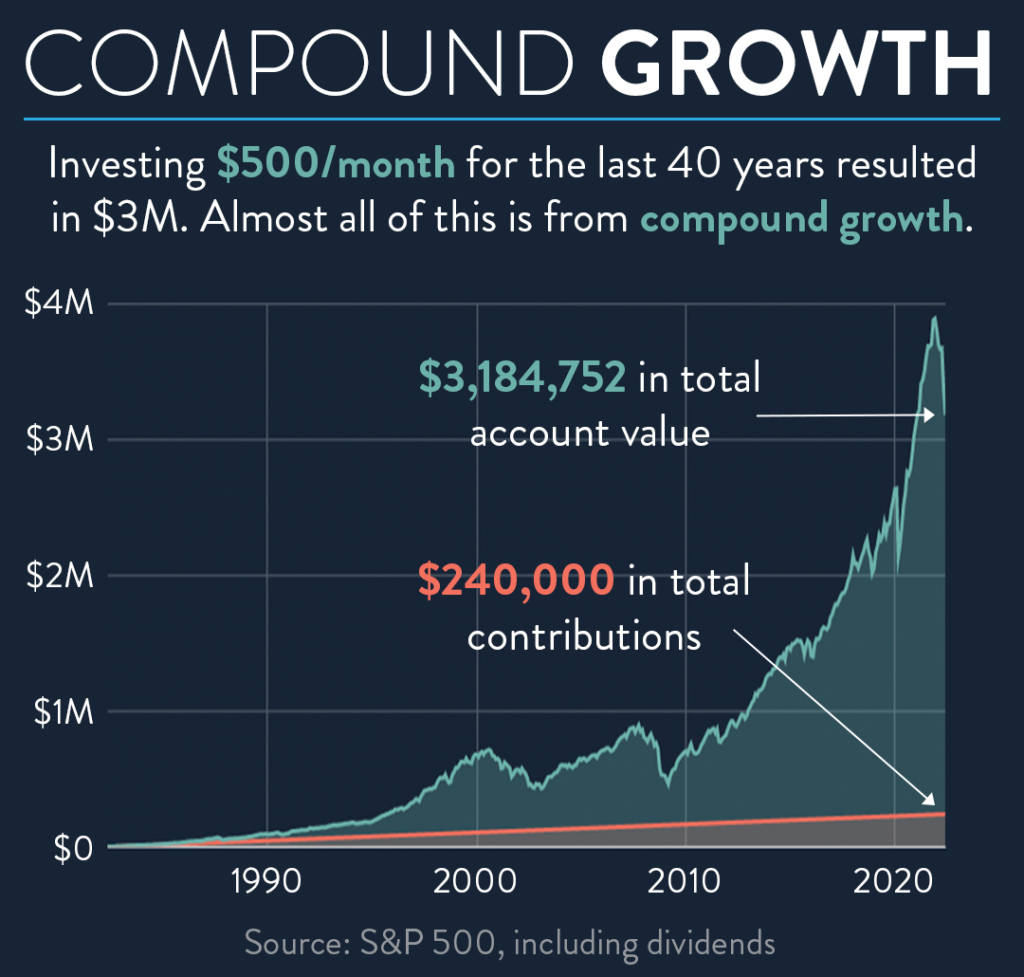

The power of compounding: Money invested early has more time to compound, which is why starting is almost always more important than optimizing. An individual who invests consistently starting in their twenties, even in modest amounts, will typically outperform someone who waits until their forties to begin, even if the latter invests larger sums — simply because of the extra decades of compounding growth.

The Hard and Soft Answers to Achieving Wealth

How do you actually achieve wealth? There are two honest answers to this question — a hard, monetary answer, and a soft, psychological one — and both matter more than most financial content acknowledges.

The hard answer is the mechanical one we’ve covered so far: know your net worth, set goals, budget, save, eliminate debt, and invest. These are the levers you can pull, measure, and optimize.

The soft answer is less discussed but equally decisive: wealth is also a psychological state. If your financial affairs are not in order — if you don’t know your net worth, haven’t written down your goals, and have no functioning budget — it becomes very difficult to genuinely believe you’ve achieved a wealthy life, regardless of your bank balance. Disorganization creates anxiety even in the presence of assets. Clarity, by contrast, creates a sense of control and security that is itself a core component of what most people actually mean when they say they want to be “wealthy.”

This is why implementing a written financial plan matters so much, even for people who feel they haven’t made much progress yet. If you haven’t assembled a plan — or haven’t even thought seriously about how to manage your financial future — you are not alone. Most people are, by nature, imperfect planners. The task is simply to begin, and to continue as consistently as possible, whether independently or with professional guidance.

It is worth dwelling on the psychological side a little longer, because the fintech and investment industry often undersells it. Money stress is rarely just about the size of a bank balance — it is very often about ambiguity. Not knowing exactly how much debt you carry, not knowing whether you’re on track for retirement, not knowing whether an emergency would derail your life for months — this ambiguity is exhausting in a way that a precisely known, even modest, financial position simply is not. Two people with identical net worth can experience radically different levels of financial anxiety, purely as a function of how clearly each of them understands their own numbers.

This is also why the very first step of this guide — calculating your net worth — carries psychological weight far beyond its arithmetic simplicity. The act of writing down every asset and every liability, in full, is often the single most anxiety-reducing exercise a person can do with their finances, regardless of whether the resulting number is impressive. Clarity, in other words, is not merely a tool for better decision-making. It is itself a form of wealth.

The Four-Pillar Lifetime Wealth Framework

Beyond the six practical steps, professional wealth managers organize the entire lifetime arc of financial planning into four sequential pillars. Understanding this framework helps you see where you currently sit in your own financial journey, and what comes next.

1. Protect

Safeguard your assets and income through insurance, emergency reserves, and risk management before aggressively pursuing growth.

2. Accumulate

Build monetary wealth through disciplined saving, career growth, and consistent investing over your working years.

3. Defend

Preserve accumulated wealth against inflation, market volatility, taxes, and unexpected life events as your asset base grows.

4. Distribute

Deploy your wealth during your lifetime for yourself and your family, and structure its transfer to heirs after death.

Notice the sequence: protection comes before accumulation, and accumulation comes before defense and distribution. Many individuals attempt to skip straight to aggressive investing (accumulation) without first protecting their income and building a safety net — a sequencing error that can undo years of progress in a single adverse event, such as a disability, lawsuit, or medical emergency without adequate insurance coverage.

The Six-Step Professional Financial Planning Process

As put forward in the Certified Financial Planner Board of Standards’ Financial Planning Practice Standards, there are six formal steps in the professional personal financial planning process. Even if you never hire a CFP, understanding this process is valuable, because it shows you exactly how a professional would approach your finances — and gives you a model to follow as your own do-it-yourself planner.

- Establishing and defining the relationship with the financial planning client — clarifying scope, expectations, and responsibilities.

- Gathering client data and determining the client’s goals and expectations in detail.

- Determining the client’s financial status by analyzing and evaluating all gathered information — essentially, calculating net worth and cash flow in depth.

- Developing and presenting the financial plan — the concrete recommendations across budgeting, saving, debt, insurance, and investing.

- Implementing the financial plan — opening accounts, automating contributions, restructuring debt, and executing recommendations.

- Monitoring the financial plan — reviewing progress on a regular schedule and adjusting for life changes, market conditions, and evolving goals.

These six steps are designed for professional CFP certificants, but several of the underlying tasks apply directly to any individual beginning the financial planning process independently — starting with gathering your financial and personal records, which we cover next.

Working with a professional accelerates every one of these steps. Whether you plan independently or with guidance, becoming an educated, engaged participant in your own financial planning process is what separates people who build lasting wealth from people who simply hope for it.

Financial Record-Keeping: What to Keep and For How Long

Good personal record-keeping has one obvious but underrated advantage: it tells you, with certainty, where and how your money is currently moving. These records are the raw material for your budget, and they establish your true financial starting point — you cannot begin the journey of financial planning without first knowing where you stand.

There is no single universal answer for exactly which documents to retain or for how long, since this depends partly on personal preference and jurisdiction. However, professional guidance generally converges on the following principles.

| Document Type | Recommended Retention |

|---|---|

| Insurance policies | Indefinitely (while active) |

| Brokerage account statements | Indefinitely, or per cost-basis needs |

| Mortgage statements, deeds, and leases | Indefinitely |

| Notes receivable | Indefinitely until settled |

| Retirement plan statements (vested amounts) | Indefinitely |

| Personal income tax returns | Minimum 3 years (many experts recommend longer) |

No single document tells you more about your financial life than your annual income tax return. It forces disclosure not only of how much you earned, but where that income came from — an extremely important input for both budgeting and long-term financial planning. Many jurisdictions legally require retention of tax returns and supporting documentation for a minimum period (commonly around three years from the relevant filing deadline), but given how much financial history a return captures, many professionals recommend retaining copies well beyond that legal minimum.

Once you’ve determined what to keep, decide where to keep it. There’s no single correct answer, but records — especially those containing sensitive personal and financial information — should be stored securely, whether in a fireproof physical location, an encrypted digital vault, or both.

Common Financial Goals Individuals Plan For

Every financial plan is different, but certain goals appear again and again across conversations between individuals and financial planners globally. Reviewing this list can help you identify which goals are most relevant to your own life stage and priorities:

- Retiring early, or retiring at a normal age with an adequate, sustainable level of income

- Funding a child’s (or children’s) college or university education

- Buying a primary home or a vacation property

- Making significant home improvements

- Taking a major, once-in-a-lifetime vacation

- Reducing or eliminating debt service, such as paying off outstanding credit card balances

- Purchasing a luxury vehicle

- Minimizing income tax or estate (transfer) tax exposure

- Starting or scaling a business

The value of this list isn’t that you should pursue all of these goals — it’s that seeing them laid out helps you recognize which ones genuinely matter to you, versus which ones you may have absorbed as generic expectations without examining them closely. A financial plan built around goals that are authentically yours is far more sustainable than one built around goals you feel you’re “supposed” to have.

How Fintech Has Changed the Financial Planning Process

The six practical steps outlined earlier — net worth, goals, budgeting, emergency savings, debt payoff, and investing — are not new. What has changed dramatically over the past decade is how accessible the tools for executing them have become. A process that once required a filing cabinet, a paper ledger, and periodic meetings with a bank manager can now be substantially automated through a smartphone.

Net worth tracking

Modern account-aggregation platforms can pull balances from checking, savings, credit, investment, and loan accounts into a single dashboard, updating your net worth calculation automatically rather than requiring manual recalculation. This removes the single biggest friction point in Step 1 — the tedium of gathering figures from a dozen different institutions.

Budgeting and cash-flow visibility

Digital budgeting tools now categorize transactions automatically, flag unusual spending, and forecast upcoming cash flow based on historical patterns. This turns the traditionally manual, error-prone process of budget-building described in Step 3 into something closer to a real-time dashboard than a monthly chore.

Automated saving and investing

“Pay yourself first” — the core budgeting principle behind a healthy emergency fund and consistent investing — is now largely automatable. Round-up savings tools, scheduled transfers, and automated portfolio rebalancing mean the discipline required to execute Steps 4 through 6 has shifted from constant manual effort toward a one-time setup decision, followed by periodic monitoring.

Debt optimization

Fintech platforms increasingly offer built-in debt-payoff calculators that model the avalanche and snowball methods side by side, showing the exact time and interest savings of each approach before you commit — turning what used to be a rough manual estimate into a precise, personalized projection.

The takeaway for a global audience: Technology has not changed the underlying principles of financial planning — it has changed the cost of executing them well. The frameworks in this guide remain the same ones taught by CFP professionals; what’s different is that individuals now have institutional-grade tools available at little or no cost, in nearly every market worldwide.

Common Mistakes That Derail a Financial Plan

Even well-intentioned individuals with a clear plan often stumble in predictable ways. Recognizing these patterns in advance is one of the most effective forms of protection you can build into your own financial planning process.

Mistake 1 — Skipping the emergency fund to invest faster

Chasing higher investment returns before building any cash cushion is one of the most common sequencing errors. When an unexpected expense hits an investor with no emergency fund, the typical response is to sell investments at an unplanned, often unfavorable moment, or to rely on high-interest credit — undoing months or years of progress in a single event.

Mistake 2 — Setting goals without attaching numbers or deadlines

A goal like “save for retirement” provides no way to measure progress or know when you’re on track. Every goal in your plan should have a target amount and a target date attached, even if both are rough estimates that get refined over time.

Mistake 3 — Letting lifestyle inflation absorb every raise

As income grows, spending very often grows to match it — a pattern sometimes called lifestyle inflation. Without a deliberate rule (for example, automatically directing a fixed percentage of every raise toward savings and investing before it reaches your everyday spending account), rising income can fail to translate into rising net worth at all.

Mistake 4 — Treating debt payoff and investing as mutually exclusive

Many individuals wait until all debt is completely eliminated before contributing anything to investments, even when an employer offers a matching retirement contribction. In most cases, capturing a full employer match while simultaneously paying down high-interest debt produces a better overall outcome than pursuing either goal in strict isolation.

Mistake 5 — Never revisiting the plan

A financial plan built once and never reviewed again slowly drifts out of alignment with reality as income, expenses, family circumstances, and markets change. The sixth step of the professional CFP process — monitoring the plan — exists precisely because a plan is a living document, not a one-time deliverable.

Your Financial Health Checklist

Use this checklist as a quick, practical audit of where your own financial plan currently stands. It condenses every step covered in this guide into a single actionable reference.

| Checklist Item | Status to Aim For |

|---|---|

| Net worth calculated and documented | Recalculated at least quarterly |

| Written SMART financial goals | Short-, medium-, and long-term goals defined with numbers and dates |

| Monthly budget in place | Income and expenses tracked; goals built into allocations |

| Emergency fund | 3–6 months of essential expenses, held in liquid savings |

| High-interest debt | Active payoff plan using avalanche or snowball method |

| Investment accounts | Retirement account funded; portfolio diversified to risk tolerance |

| Insurance coverage | Health, life, and income protection reviewed annually |

| Financial records | Organized, securely stored, retained per guidance above |

| Plan review cadence | Full review scheduled at least once per year |

A Global Perspective: Financial Planning Across Markets

One of the strengths of the framework in this guide is that its core logic — net worth, goals, budget, emergency fund, debt payoff, investing — holds true regardless of geography, currency, or local regulation. What changes from market to market is not the framework itself, but the specific instruments available to execute it.

In some markets, tax-advantaged retirement accounts function similarly to an IRA; in others, employer-sponsored pension schemes or government-backed provident funds play a larger role in the accumulation pillar. Emergency fund guidance of three to six months of expenses applies broadly, though individuals in markets with weaker social safety nets, less job security, or higher currency volatility may reasonably extend that target further. Debt structures also vary significantly — some markets carry very high consumer credit card rates, making the debt avalanche method especially valuable, while others rely more heavily on lower-rate installment lending.

What does not vary is the discipline required. Whether you are building wealth in a mature, highly regulated financial market or in a fast-growing, digitally-native fintech ecosystem, the same six steps and four pillars apply. This is precisely why the framework in this guide is designed to travel — as an SOP document, a training reference, or a presentation framework — across markets, languages, and financial systems worldwide.

For financial educators and fintech professionals: This structure is intentionally modular. Each step, pillar, and process can be localized with market-specific instruments, tax rules, and regulatory detail while preserving the same underlying architecture — making it well suited for training programs, onboarding content, and investor education initiatives across multiple regions.

Turning This Guide Into Action

Financial planning is not a single event you complete and move on from — it is an ongoing discipline, revisited and refined as your income, goals, and life circumstances evolve. The six practical steps in this guide — determining net worth, setting SMART goals, budgeting, building an emergency fund, eliminating debt, and investing — form the operational core of that discipline. The four-pillar framework of protecting, accumulating, defending, and distributing wealth gives that discipline a lifetime structure. And the six-step CFP process, along with disciplined record-keeping, gives you the same rigor a professional planner would bring to your finances.

None of this requires perfection on day one. It requires a starting point, a written plan, and consistency over time. Whether you choose to manage this process entirely on your own, or to become an educated consumer working alongside a professional financial planner, the single most important action available to you right now is simple: begin.

Print this guide, bookmark it, or save it as a standing reference document. Revisit it at each major life transition — a new job, a marriage, a child, a home purchase, a career change — because each of these moments changes your numbers, your goals, and often your risk tolerance, without changing the underlying framework you use to plan around them. That durability is the point. A good financial plan isn’t rewritten from scratch every few years; it is the same structure, recalibrated with new inputs, carried forward for a lifetime.

Ready to put this framework into practice?

Start by calculating your net worth this week — it is the foundation every other step in this guide depends on.

Revisit Step 1: Determine Your Net WorthFrequently Asked Questions

What is the first step in financial planning?

The first step is determining your net worth by subtracting total liabilities from total assets. This establishes an accurate starting point before you can set meaningful goals or build a budget.

How much should I keep in an emergency fund?

Most professional guidance recommends three to six months of essential living expenses, held in a liquid, easily accessible savings account rather than invested in the market.

Should I pay off debt or invest first?

Generally, high-interest debt (such as credit card debt) should be prioritized before aggressive investing, since the interest rate on that debt often exceeds typical long-term investment returns. Retirement contributions that receive an employer match are often a reasonable exception worth pursuing alongside debt payoff.

What are SMART financial goals?

SMART goals are Specific, Measurable, Achievable, Relevant, and Time-bound. This structure converts vague ambitions like “save more” into concrete, trackable targets with real numbers and deadlines attached.

How long should I keep my tax returns?

Most jurisdictions require retention for a minimum of around three years from the filing deadline, though many financial professionals recommend keeping returns significantly longer given how much financial history they document.

Do I need a financial planner, or can I do this myself?

Both approaches are viable. Many individuals successfully manage their own financial planning using a structured process like the one in this guide, while others benefit from professional guidance — particularly as finances become more complex. Becoming an educated, engaged participant in the process is valuable either way.